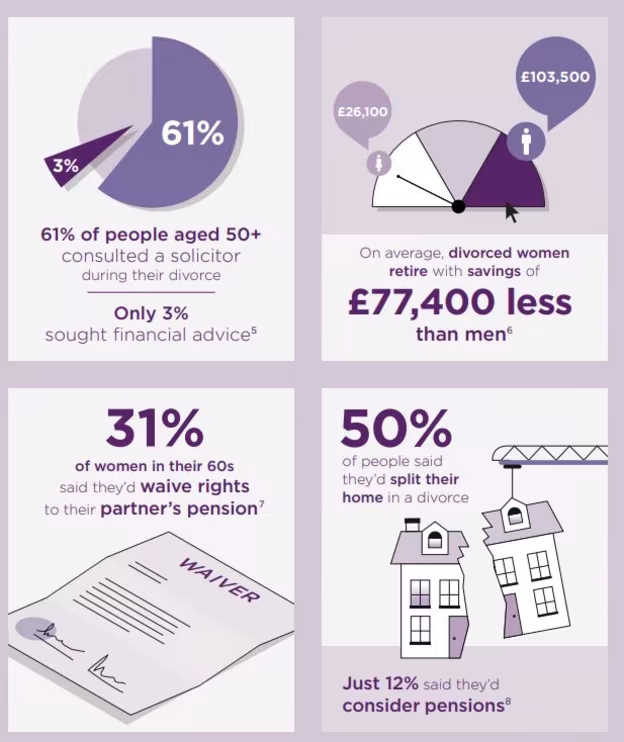

Spike in divorce rate increases risk of financial vulnerability

The Financial Vulnerability Taskforce has launched a good practice guide to highlight the range of vulnerable circumstances arising from the impact of divorce.

The guide, titled Advising and supporting clients going through Divorce (in England and Wales), focuses on immediate and future vulnerable circumstances and the need for professional advice.

In April 2022, the Divorce, Dissolution and Separation Act 2020 came into force across England and Wales, enabling married couples to issue divorce proceedings without assigning blame.

According to The Law Society, this has resulted in a spike in no-fault divorce applications, contributing to delays and backlogs in the civil law courts.

Keith Richards, chair of the FVT, said: “Whilst the change in law removes bureaucracy and cost, the unintended consequences may be increased financial vulnerability.

“Collaboration between financial advisers and the legal profession is at the heart of good outcomes for clients going through separation and divorce, and experts from both professions have contributed to this guide.”

A core purpose of the taskforce is to encourage greater collaboration between financial planning and related professional services, including legal, tax and accountancy.

Tony Miles, author of the guide and a founding board member of the FVT, said: “The provision of relevant financial advice to clients going through separation or divorce is a complex matter, and not necessarily a core part of most financial advisers’ client services.

“We hope this new guide will encourage financial advisers to work closely with other professionals with relevant expertise, to help ensure that parties going through the difficult matter of a divorce benefit accordingly, and increasingly see the advisory profession as a safe pair of hands.”

The guide outlines the procedure step by step for advisers navigating clients through divorce. It outlines the timeline and cost of a divorce process, dealing with money and property and the legal principles, as well as dealing with income and spousal maintenance.

It highlights key documentation required such as the financial settlement, statement of information for a consent order, pension enquiry form information and state pension enquiry.

The guide says there are multiple ways that a client can go, one is the do-it-yourself route, where both parties go through the divorce and financial negotiation process with little or no help from a solicitor.

Another is family mediation which is a process in which an independent, professionally trained mediator helps both parties work out arrangements for children and/or finances following separation.

Considering the role of a financial adviser, it said that some advisers specialise in divorce work, but all of them can play a significant role in supporting their clients going through a divorce or separation, and their financial wellbeing after the event.

“By the very nature of their role, financial advisers and planners tend to have lengthy and ongoing relationships with their clients, and can be viewed by many as trusted friends,” it said. “In practical terms, such a role can complement and add value to the role of other professionals, helping all parties get a broad picture of their financial position, helping them navigate the financial elements of the divorce process, as well as assisting with financial matters post-divorce.

“Instead of acting in an advice and adversarial capacity for one party, the financial planning professional might in an increasing number of cases be asked to act as a single joint expert, recommending a possible division of assets, for example to provide equality of income at a specific retirement age.”

The guide said before undertaking this type of work, it is important that the financial adviser planner should have a thorough understanding of the relevant rules and regulations.

The taskforce outlines the areas for an adviser to consider before and during divorce such as tax liability and life insurance.